Fee Proposal Tool

Asset Repositioning

Fee Calculator

Fee Summary

Ranges based on US market data 2024–2026 · Enter custom % in each fee card to override defaults

Note upfront: I'm not a tax advisor, so treat this as an educational overview and confirm specifics with your CPA.

Potential Tax Benefits — $110K Rental Income and $200K in Improvements

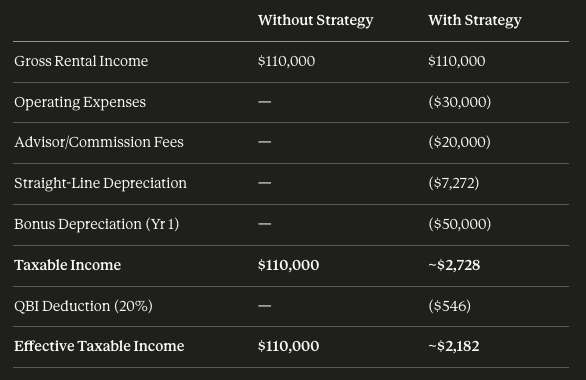

Your baseline without any strategy: $110,000 fully taxable at your ordinary income rate (22%–37% depending on bracket) = $24,200–$40,700 in taxes.

Here's what changes when you apply the available strategies:

Straight-Line Depreciation — Your $200K in capital improvements depreciates over 27.5 years under IRS rules for residential rental property. That's a $7,272 annual deduction every year, reducing your taxable income without spending another dollar. Over the full 27.5 years, that's $200,000 in total deductions on money you already spent.

Cost Segregation Study — An engineering-based analysis that breaks your $200K improvement into components by useful life. Flooring, fixtures, appliances, cabinetry, electrical, landscaping, and specialized wiring get reclassified from 27.5-year property into 5-, 7-, or 15-year buckets. On $200K of improvements, studies typically identify 20–30% as short-life assets — meaning $40,000–$60,000 gets pulled out for accelerated treatment. Studies run $5K–$15K and almost always pay for themselves on an improvement of this size.

Accelerated Bonus Depreciation (100% — restored in 2025) — This is the most powerful current benefit. The One Big Beautiful Bill Act permanently restored 100% bonus depreciation for qualified property placed in service after January 19, 2025. Any short-life assets identified in your cost segregation study — those 5-, 7-, and 15-year components can be fully expensed in Year 1 instead of being spread over decades. On your $200K improvement, if $50,000 is reclassified as short-life assets, that's a $50,000 deduction in the first year alone, on top of your regular depreciation.

Operating Expense Deductions — Every dollar you pay in property management fees, insurance, property taxes, maintenance, advertising, and advisory/repositioning fees is fully deductible as a business expense in the year paid. Your commissions and consulting fees from the repositioning work are deducted dollar-for-dollar — not amortized. On $110K gross income, real operating expenses typically bring taxable income down to $60,000–$75,000 before depreciation is even applied.

Qualified Business Income (QBI) Deduction — If your rental activity qualifies as a trade or business (or meets the IRS safe harbor test), you can deduct an additional 20% of your net qualified business income. This is one of the most frequently missed deductions for landlords. On $50,000 of net rental income after expenses and depreciation, that's another $10,000 off your taxable income permanently extended under the 2025 tax bill.

Passive Loss Allowance ($25,000 rule) — Depreciation frequently creates a paper loss even when the property generates positive cash flow. If you actively participate in managing the property and your adjusted gross income is under $100,000, you can deduct up to $25,000 of that passive loss against your W-2 or other ordinary income. This phases out between $100K–$150K AGI. If you or your spouse qualify as a Real Estate Professional, the $25K cap disappears entirely and losses are unlimited.

1031 Exchange (Exit Strategy) — When you sell, the IRS recaptures all depreciation at 25% — so planning your exit matters as much as the entry. A 1031 exchange lets you roll your gains into a replacement property tax-deferred, indefinitely. Combined with the depreciation benefits above, this is how serious real estate investors build generational wealth without triggering large tax events.

What Your Numbers Could Look Like

In Year 1 alone, you could go from paying taxes on $110,000 down to nearly $0 in taxable rental income while the property still generated positive cash flow. That's the power of stacking depreciation, bonus expensing, and operating deductions together.

Let’s Work Together

If you're interested in working with us, complete the form with a few details about your project. We'll review your message and get back to you within 48 hours.